Explainer: Who Can Now Benefit From US Tax Equity Policy?

In Brief

Investment and production tax credits go to a wider range of entities now.

Cities and nonprofits can use them to build renewable power systems.

This explainer lays out who can do what with which credit where.

With the August 12 announcement of the Inflation Reduction Act comes thunderous optimism: “The Senate Inflation Reduction Act could cut annual emissions in 2030 by an additional ~1 billion metric tons; could close two-thirds of the remaining emissions gap between current policy and the nation’s 2030 climate target of 50% below 2005; reduce cumulative GHG emissions by 6.3 billion tons over the next decade” according to Princeton University’s ZERO (Zero-carbon Energy Systems Research and Optimization Laboratory).

Two core incentives take center stage to enhance the market penetrability of renewable energy under the IRA: Investment Tax Credit (ITC) and Production Tax Credit (PTC). What are the ITC and PTC? Who is eligible? What are the revisions made under the IRA? If these questions sound familiar, this explainer is for you.

The ITC and PTC have appeared in the United States’ tax code since the 1978 Energy Tax Act and 1992 Energy Policy Act, respectively. As revised under the IRA, they can significantly cut the costs of eligible clean energy businesses by slashing tax liabilities. If you are an energy developer looking to finance clean energy projects, you have to choose one of each per project.

The ITC is a one-time, lump-sum percentage rebate applied to investment in businesses and assets whose eligibility is enforced under the discretion of the IRS. If you’re a solar developer eligible for an ITC of 10% under the guidance of the IRA, you can raise cash by selling a flat, 10% reduction in total tax liability to investors - an attractive option for developers handling projects with high upfront capital costs.

The PTC whittles down your tax liability by applying sustained rebates for every unit of production. For example, the rebate may be phased in at a fixed amount per kilowatt hour of clean energy production generated by your business (let’s say, 3 cents per kilowatt hour of solar energy), providing tax credits proportional to output capacities over time.

Developers without sufficient tax liabilities to realize the full value of these credits can sell these credits through credit transfers to help finance the project.

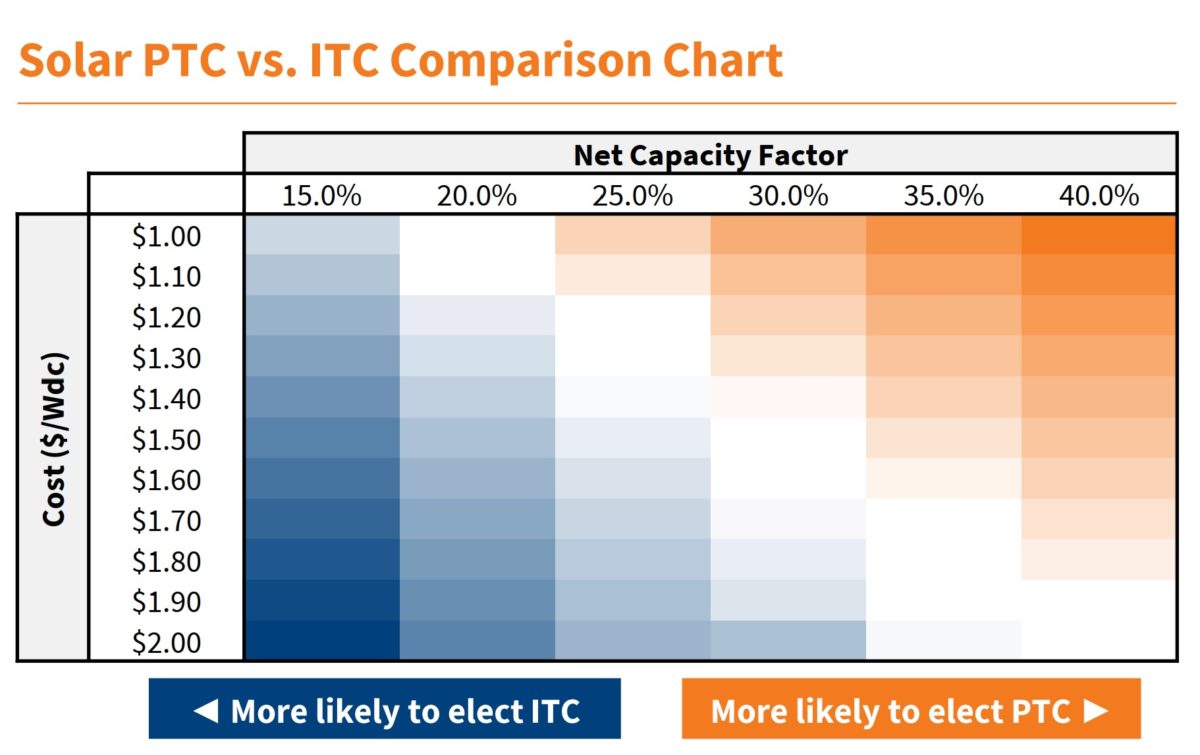

So, which to choose? We consult the analysis of CohnReznick Capital, an assurance, advisory, and tax firm based in New York:

On the Y axis we have the cost factor: what is the upfront cost of the project? The X axis considers the net capacity factor: what proportion of its capacity does the plant or project generate? We can then abstract two likelihoods: if the project requires large initial capital cost and has a low sustained production capacity, the ITC is likely to capitalize the project; if the project requires low initial capital cost and has high production output, the PTC is likely to be preferred.

Revisions under the IRA

Referencing Foley & Lardner LLP’s analysis of the IRA, we now investigate the core revisions made under the IRA concerning the ITC and PTC.

The pool of entities that can own or sell tax credits grows under Section 45:. Projects that begin construction prior to January 1, 2025 are eligible for the PTC’s base credit amount or increased credit amount. Eligible projects create wind, closed and open loop biomass, geothermal landfill gas, trash, qualified hydropower, marine, and hydrokinetic facilities, with some qualifications. Investors can take PTCs for a full 10 years from the day a solar project comes online.

Financing for projects underway or for projects that start construction within 60 days of the IRS’ final guidance on the IRA can draw on the tax credit. Later projects must be small or must pay prevailing wages and set up formal training programs, called apprenticeships, to apply for the credits.

For bonuses, the key is domestic content requirements. To qualify for a 10% increase, developers have to use American-made steel and iron. They also have to show that at least 40% of the facility’s parts come from the United States or one of its trading partners. The IRS is developing guidance on how to interpret these rules.

Changes to ITC applicability look similar, those eligible projects also include solar, fiber-optic solar, qualified fuel cell, qualified microturbine, combined heat and power system, qualified small wind, and waste energy recovery properties. It also applies tax credit eligibility to standalone energy storage, qualified biogas property, electromechanical fuel cells, dynamic glass, and microgrid controllers.

The eligibility requirement for base and increased credit amounts for the ITC is likewise applicably similar to that of the PTC. If you have facilities that broke ground 60 days after the IRS’s guidance about the Act Beginning Construction Deadline, or if you possess facilities that have begun service in 2022 or broke ground prior to the Act Beginning Construction Deadline, you may be eligible for the 30% credit amount. If you have projects that will break ground after the Act Beginning Construction deadline, the eligibility requirements are the same as those of the PTC (maximum output of facility less than 1MW(AC), or satisfy prevailing wage and apprenticeship requirements). The ITC percentage will be diminished to 6% if you fail to meet those requirements.

Perhaps because more developers market ITCs than PTCs, Congress increased the domestic content requirements for that credit to 50 percent and trimmed the credit availability for projects that start down the line.

Direct pay and credit transfer

Direct pay and credit transfer options relieve developers - including nonprofits and public sector players - from the trouble of finding investors who are trying to shrink tax bills by enabling refunds and sales to realize the value from credits. The direct pay option permits states, cities and local municipalities, tribes and other tax-exempt entities to claim the benefits of the ITC and PTC through proportionate cash payments (since they have a tax liability of $0) and credit transfers (the sale of credits to unrelated taxpayers for cash) as long as they meet the prevailing wage and apprenticeship requirements. In short, eligible entities can now refund or transfer credits to monetize and fuel their businesses.

Direct pay can also apply to carbon capture and other less mature technologies, with the same requirements for training and domestic content.

The transferability provision creates a limited marketplace of credits for sellers who do not have tax liabilities they can offset through tax credits, and for buyers who have sufficient tax liabilities they can offset. This allows the values of the ITC and PTC to permeate the market with greater flexibility - even if the initial recipient cannot benefit from a reduction of tax bills, they can trade their rebate to another entity that will benefit from the intended value of the subsidy. However, the credit transfer option isn’t without its caveats: first, the buyer of a credit is forbidden from deducting the cost of said credit, nor is the cash gained by the seller recognized as income; second, the buyer of the credit is forbidden from selling the credit - in part or in whole - to other taxpayers. A failure to conform to these guidelines can result in penalties.

The budgetary proportioning under the Inflation Reduction Act reaffirms the significance of taxes as formidable tools through which a sustainable United States can be consummated. The PTC and ITC are still subject to IRS guidance and establishment of precedents, but the promise they carry deserves commitment from developers and investors.